Few in the U.S. Virgin Islands are unaware that the V.I. Government Employees’ Retirement System is losing money and that there is a proposal to cut some benefits very sharply in 2021. The situation, all acknowledge, is dire.

Right now, Gov. Albert Bryan Jr. has two proposals before the Legislature that are intended to help. One devotes potential future cannabis revenues to GERS, and the other hopes to please lenders and enable the government to save money by refinancing debts and devoting some of the savings to GERS.

Nothing Bryan or anyone else has proposed is big enough to plausibly prevent the collapse and sharp cuts in benefits. But acting sooner rather than later can still soften the blow and preserve some semblance of a pension system into the future.

This V.I. Source series will look at how we got here, what it means to retirees, past efforts at reform, current proposals, suggestions to fix the problem and their likelihood of success and whether there may be other, not-yet proposed possibilities with some merit.

How Bad Is It and How Did We Get Here?

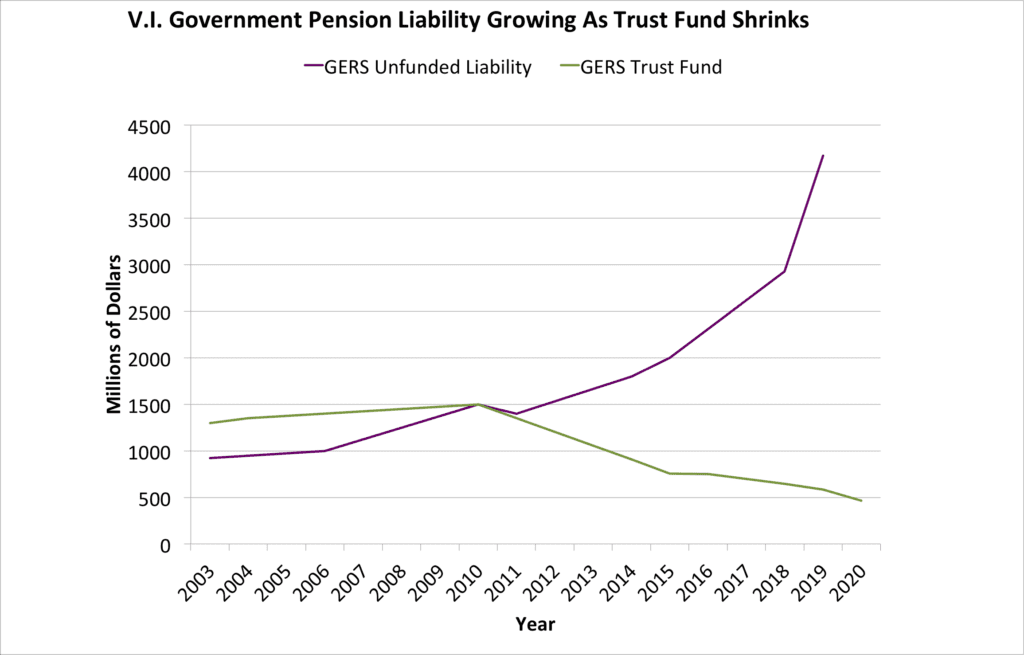

Today, the V.I. pension trust fund is rapidly dwindling and as of Sept. 30, 2019, had an unfunded liability of $4.172 billion. Its assets and projected income are less than 16 percent of the total liability for present and future pensions.

As far back as 1998, our first year of publication, the Source reported the V.I. government pension system was giving out more in benefits than it was collecting in contributions.

That year, GERS gave out $11.7 million more than it took in and projected an unfunded liability – pension payments it would not be able to pay – of about $518 million. GERS Administrator Austin Nibbs has told the Legislature that pension payments first exceeded contributions and earnings two years earlier, in 1996.

But the pension system was already in a serious crisis years before that, strained by V.I. Legislature-mandated benefit increases without contribution increases to fund future obligations.

The V.I. government “has not been paying its actuarially determined contributions since 1992,” Nibbs said in a recent interview. In each of the 28 ensuing years, GERS officials have sounded the alarm multiple times a year, pointing to the problem every time they appeared before the Legislature and at regular public meetings.

But there has been little political will to make painful changes. When reforms were proposed, they were too mild to address the problem. As the severity of the crisis became more and more apparent and the alarms got louder and louder, governors and senators began to enact changes, but again, too little too late. Frequently, the government weakened or delayed the reforms it enacted or failed to carry them out due to financial constraints.

For a few years, solid returns on a billion-plus investment portfolio allowed the trust fund to continue to grow in total dollars, but with a growing projected unfunded liability.

By 2003, GERS officials were looking into the future at a projected $732 million in unfunded pensions unless sharp increases in contributions were enacted right away.

By 2006, the unfunded future pension payments came to over $1 billion, and the GERS trust fund had a market value of $1.2 billion. At this point, it was starting to spend more of its trust fund than it was earning on investments and the trust fund began to shrink.

By 2011, the unfunded liability stood at more than $1.4 billion. GERS was selling more and more of its portfolio to meet current benefit payments.

The trust fund has been shrinking by about $70 million to $100 million per year. It shrank by $72 million from 2013 to 2014, despite good investment performance. It shrank an additional $128 million from 2014 to 2015, with investment losses of $28 million, according to GERS’ budget testimony.

As of January 2016, the trust fund had shrunk to $751 million, not counting many tens of millions of dollars in real estate and millions of dollars in outstanding loans.

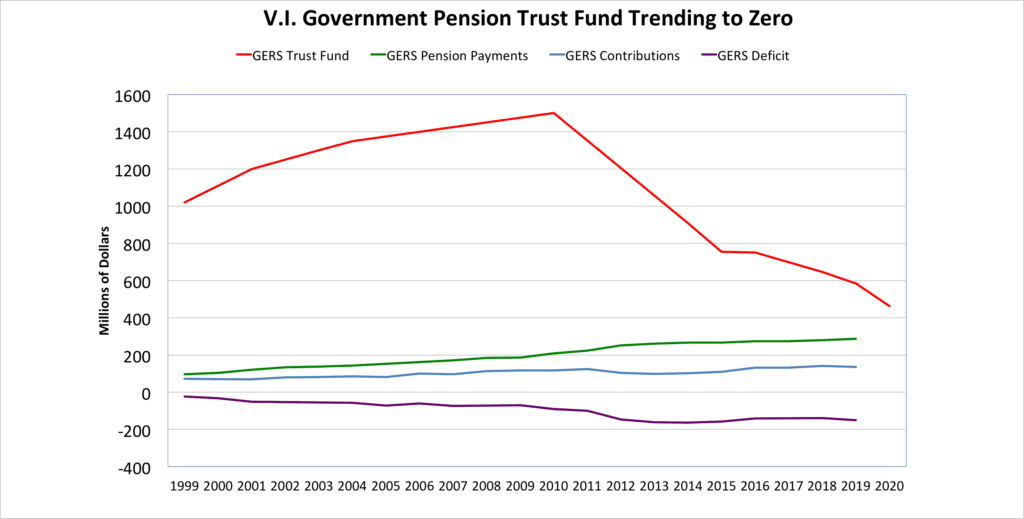

As of Sept. 30, 2020, the trust fund has $463.1 million in liquid, or cashable assets, and around $63 million in real estate, Nibbs said.

“We draw down $130 to $140 million from our assets every year,” Nibbs said.

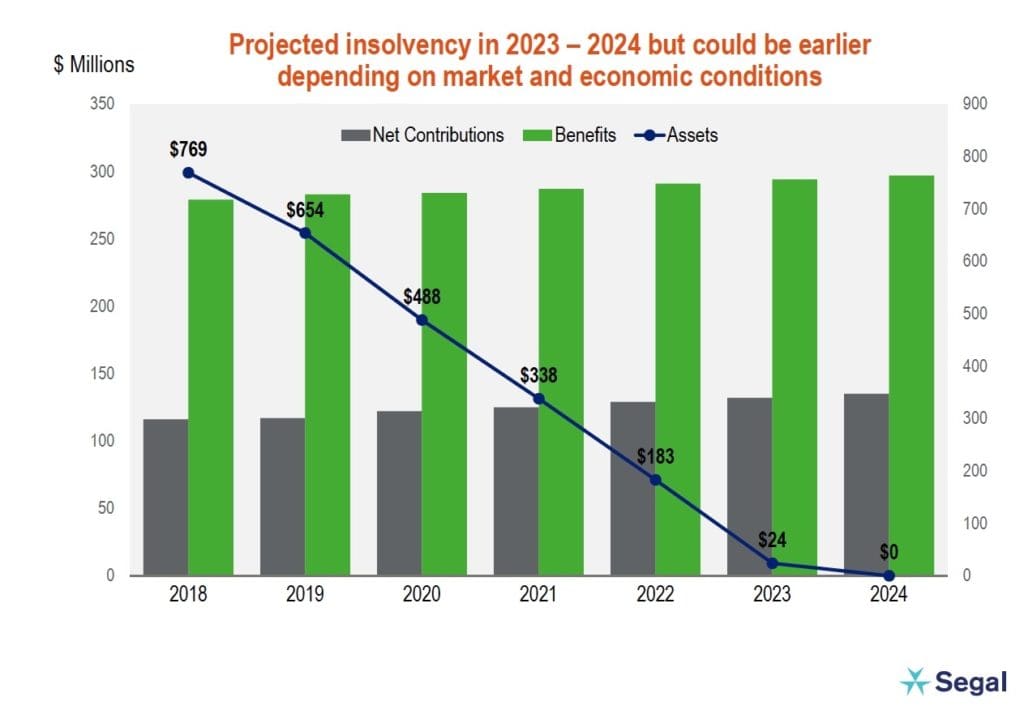

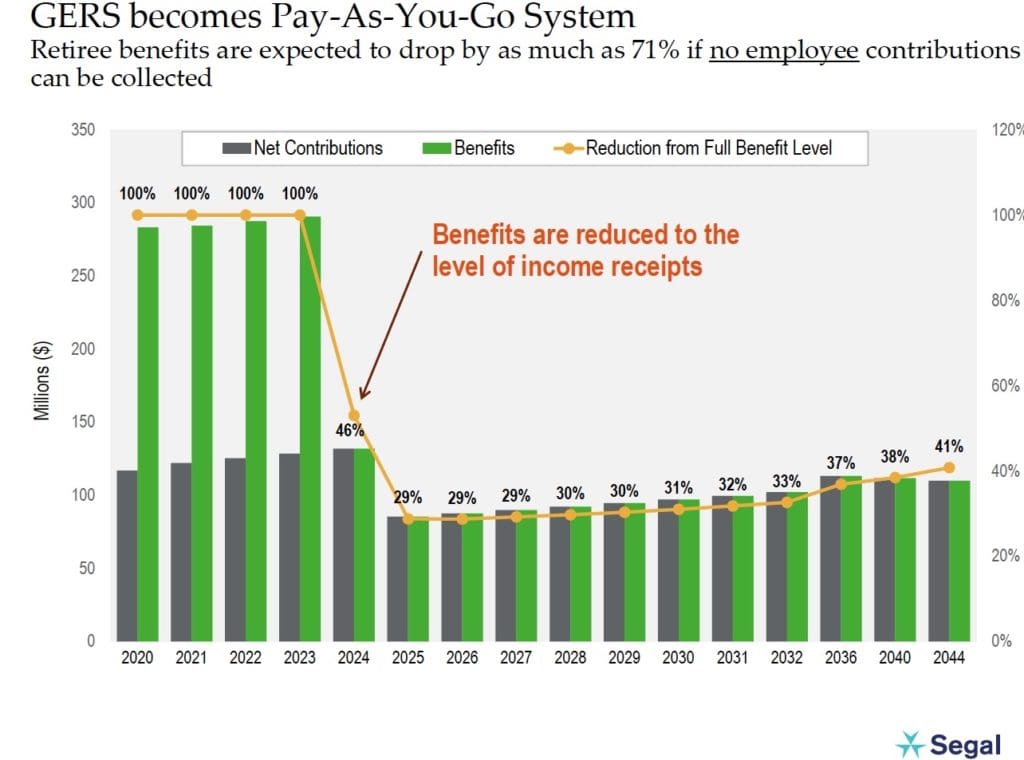

Without something to generate a new $130 to $140 million per year devoted just to GERS, the trust fund will drop to zero in less than four years, at which point there will be zero investment earnings and 100 percent of what retirees get each month will have to come from that month’s employee and employer contributions to the plan.

In May, GERS proposed a 42 percent cut for most older beneficiaries, starting in 2021, intending to avoid total collapse and hopefully preventing even harsher cuts of 55 percent or higher. Those hired after 2005, who are already due smaller pensions than earlier GERS members, would not be impacted.

If government employees can pull out of GERS, “then retirees might see a 71 percent cut,” Nibbs said.

“Their argument would be, why are you taking money out of my check and I’m not going to get a pension,” he said. According to a recent report from Segal Consulting, that assumes the 71 percent cut would be across the board, impacting all retirees, not just the higher-paid, older tier one.

Upcoming installments of this series will look at proposed reforms and possible solutions. But first, how did we get here?

Two Forces Drive the Crisis

There are two main drivers of the GERS crisis. One is a declining ratio of active employees to retirees, and another is a series of actions and inactions that led to contribution levels being too low and benefits too generous to sustain indefinitely. As pension plans persist in time there is a tendency for the number of retirees to grow, potentially more than the size of the government grows. Early retirements can exacerbate this as younger retirees continue to receive benefits for many more years.

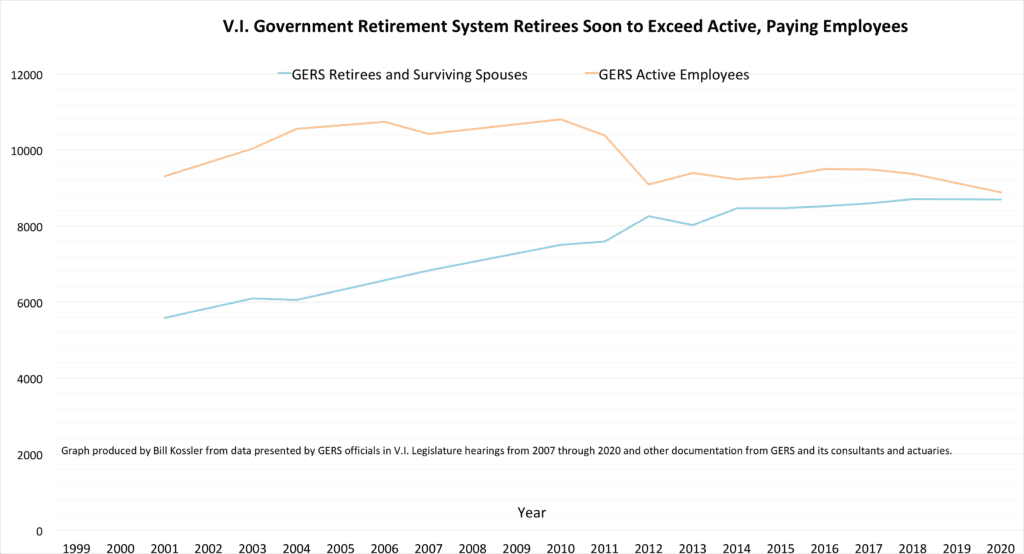

The fewer employees paying into the system, compared to the number of retirees collecting pensions, the higher contributions have to be to keep the trust fund solvent. In the 1990s, GERS had a ratio of 2.2 active employees for each retiree. That declined. A 2011 Department of the Interior Inspector General report described the ratio of retirees to employees at that time as “perilously low” at 1.4 to 1. In July 2020, there were 8,881 employees and 8,699 retirees, for a ratio of 1.02.

The other main cause of the crisis, according to the federal audit, is a series of unfunded giveaways the V.I. Legislature enacted between 1984 and 2001, aimed at encouraging early retirement to cut the workforce.

While the government “was successful in reducing its workforce, each of the laws passed either made lucrative provisions for early retirement or significantly increased benefit packages. The Legislature failed, however, to fund these retirement laws or funded them insufficiently, which has also increased the retirement system’s unfunded liability,” the federal auditors concluded. They calculate that just one of those legislative acts – the Early Retirement Incentive, Training and Promotion Act of 1994 – has prevented the collection of at least $120 million in contributions, not counting the impact of increased pension payments.

There have been multiple efforts to fix the problem. But none were close to the magnitude needed.

The most impactful action so far may have been major reforms the Legislature enacted in 2005, creating two tiers of employees. Tier I – those hired before 2005 – were to be mostly left alone, getting 2.5 percent increases in benefits per year of service and paying 8 percent of salary for their employee contributions to the pension system. Tier II, hired after 2005, would pay more in and accrue benefits slower.

But those reforms were not fully implemented until 2011. The 2011 federal audit found contributions needed to be raised to 43 percent of payroll to make the system whole at that time. Actual contributions were around 25.5 percent of the payroll.

Since then, the territory has fully implemented the two-tier system and GERS increased employer contributions by 3 percent between 2015 and 2017. In 2018, contributions amounted to 32 percent of payroll, according to GERS’ contractors Segal Consulting. GERS increased contributions by another 3 percent in 2020.

But contributions remain far below 43 percent. And since the bleeding continued for another decade, the percentage needed is now far higher.

“Last year, the figure would have been about 69.8 percent,” Nibbs said recently. Since then, he estimates it has probably increased to around 71 percent of payroll that would have to go to pension contributions to avoid collapse. “That’s if you assume a 7 percent return on investment,” Nibbs said. If you assume a more conservative 4 percent return, it would be around 91 percent of payroll, he added.

Things That Didn’t Help But Didn’t Cause the Crisis

Some major V.I. figures have pointed to other culprits, like GERS’ alternative investment program or poor investments. But those explanations fly in the face of documented facts.

Nibbs recently told senators that over the past 20 years, the market rates of return have been positive 16 out of 20 years. In many of the years, the returns were well above the assumed rate of return of 7 or 8 percent, and as high as 17.6 percent in 2003, 10.6 percent in 2004, 11.8 percent in 2005, 14.1 percent in 2007, 14.5 percent in 2012, 9.1 percent in 2013 and 11.2 percent in 2017.

GERS financial reports and independent financial audits back this up.

In 2016, then-Attorney General Claude Walker editorialized and testified to a Senate committee that he opposed giving the system any more money until greater controls were put in place. Walker pointed to a V.I. Inspector General report finding insufficient oversight over some loans and investments.

A GERS program gave out some $192 million in loans over the years. But most of the loans turned a profit. There was one large loss – a 20-year-old investment in speculative life insurance policies – that cost the system $42 million. That’s huge. But far less than the system has liquidated every year for the past decade just to pay current benefits.

Some have said GERS has spent too much on its St. Croix headquarters or paid too many consultants for too little. But even if true, the money involved is not on the same scale as the crisis.

The government has not always paid its contributions in full, which made the crisis slightly worse. In April, a federal judge ordered the V.I. government to cough up $63 million for unpaid contributions, penalties and interest, dating back to 1991. Most of that – $49 million – is penalties and interest rather than missing contributions. That is a large sum. But it too is far smaller than the amount the government has liquidated every year for the past two decades. The shortfall is measured in billions, not millions.

The V.I. government is appealing the judgment. It is also facing budget shortfalls, so any future $63 million payment will be difficult and possibly made in multiple installments over several years.

In the end, the real culprits are those federal auditors identified a decade ago, and that GERS officials were pointing to long before that. Early retirements and actuarial trends led to fewer employees covering more retirees. Contribution levels were too low to cover benefits even 30 years ago. Since then, decades of V.I. senators and other leaders have lacked the political will to take sufficiently painful and unpopular measures. And now the coffers are nearly empty.

Next: V.I. government retirees weigh in on what GERS cuts mean to them.

{kind=link}