The credit rating agency Moody’s Investor Services downgraded all V.I. government debt yet again Jan. 31, saying the territory is “highly likely” to be unable to make debt payments without restructuring. Moody’s also said the territory’s pension system may collapse “much sooner” than 2023.

The unwelcome news comes as Gov. Kenneth Mapp’s administration continues to work on persuading the federal government to extend federal disaster assistance loans to help it bridge a massive budget deficit made much worse by last year’s hurricanes.

Moody’s cites the territory’s ongoing fiscal crisis, saying the recent hurricanes have worsened the problem.

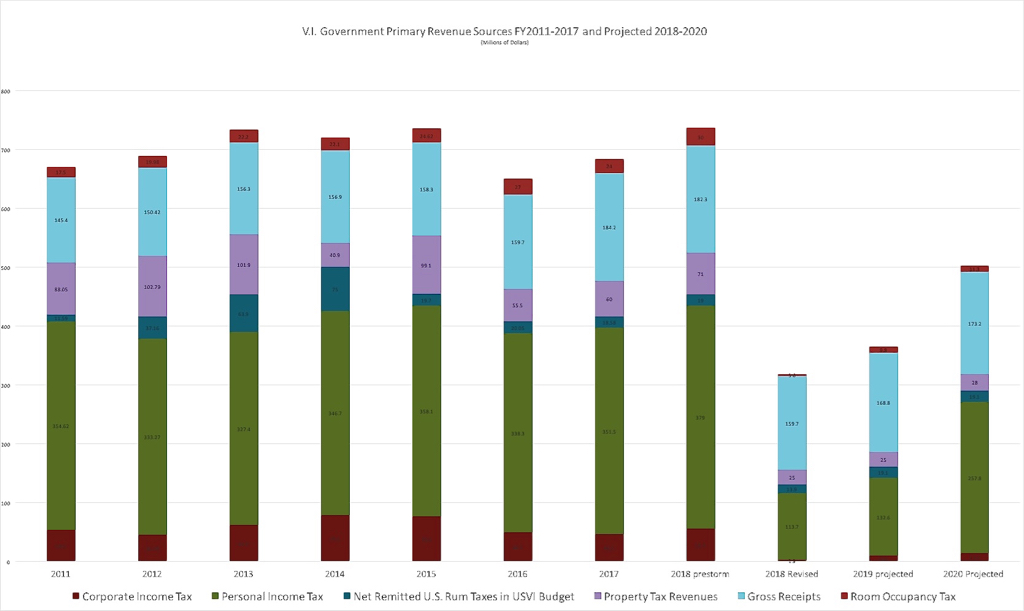

V.I. officials have told the Legislature the territory has a roughly $450 million deficit this year, up from the pre-hurricane annual $170 million structural deficit out of a locally funded budget of around $850 million. With $65 million in revenue assistance in the form of a federal disaster assistance loan, the V.I. Government should be around $385 million in the hole this year, although the actual number fluctuates as revenues and expenses fluctuate.

“While assistance from the federal government in response to the hurricanes has provided some near-term relief, we believe the severity of the territory’s fundamental fiscal and cash challenges, combined with the pending insolvency of the territory’s government employees’ retirement system, make a debt restructuring highly likely,” Moody’s analysts said in announcing the downgrade.

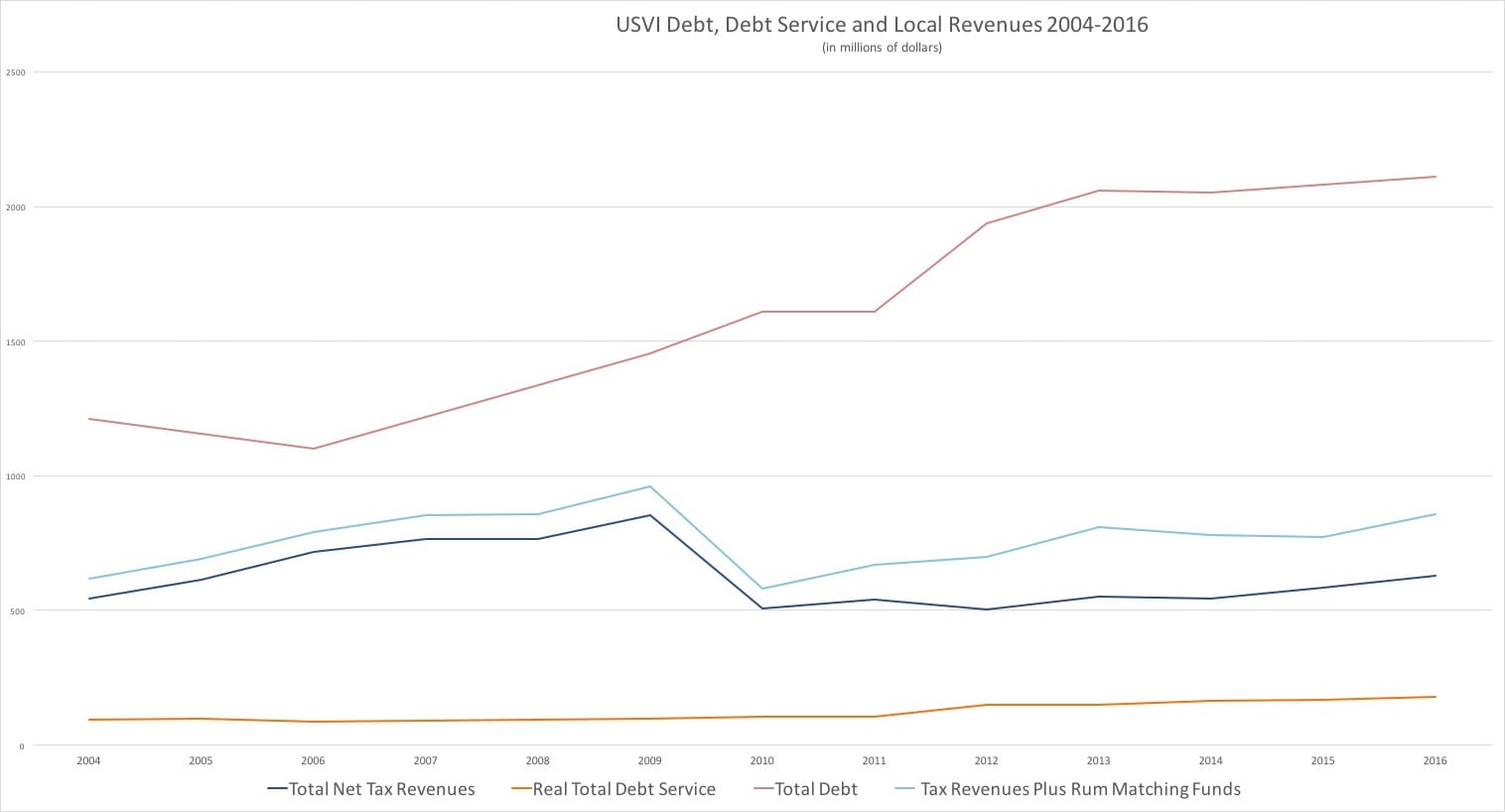

The territory has about $2 billion in outstanding debt, divided between bonds secured by territorial gross receipts taxes and “matching fund” federal alcohol excise taxes remitted to the territory.

A year ago, Moody’s adjusted USVI senior lien bonds down three full notches from the “speculative” junk rating of B1 to Caa1, which the agency terms “bonds of poor standing.” The Jan. 31 downgrade takes them down two more notches to Caa3. Moody’s has only two lower ratings: Ca, which it terms “highly speculative, or near default” and C- “bonds typically in default, little prospect for recovery of principal or interest.”

The rum industry has quickly recovered from the storms and federal excise tax revenues are projected to remain at similar levels as in recent years. But Moody’s downgraded that debt too, with senior lien debt going down to Caa2 and the rest to Caa3. Moody’s analysts say that is because if the territory has to restructure any of its debt, “matching fund bonds will inevitably be included in any debt restructuring.”

The one notch distinction between the types of matching fund debt is due to a statutory lien the government placed on revenues in 2016. The V.I. government puts local gross receipts tax revenues under the power of a special, bank-appointed trustee and federal excise tax revenues go directly to the trustee, to pay off interest and principal on V.I. bonds, before any remaining funds will go to the territory’s coffers.

The V.I. government still collects Gross Receipts taxes, so it would still have to actively deposit the funds with the trustee. The federal excise taxes are hypothetically out of the V.I. government’s hands, making them more secure for creditors. But Moody’s analysts are concerned that system is “unlikely to survive a restructuring” and “has not been tested in a stress situation in which the government attempts to divert pledged revenue for general government purposes.”

Moody’s also points to the impending collapse of the government’s pension system.

“System assets were projected to be depleted by 2023, but this will likely happen much sooner because, among other factors, the government has been deferring its statutorily-required contributions,” Moody’s analysts said.

Past-due contributions since September’s storms amount to $40 million, Finance Commissioner Valdamier Collens told senators Tuesday. That amount would be larger but the government has received $65 million in federal disaster loans dedicated to revenue assistance and put $8 million toward the pension plan.

For a sense of the scale of the shortfall, the V.I. pension system took in about $85.38 million in contributions in 2015 and paid somewhat more than $200 million in pension checks, liquidating close to $115 million from its trust fund for current expenses. The storms were five months ago in September of 2017. If the government only contributes $8 million this year, it will have to liquidate $185 million from the trust fund – double the past rate of loss. The entire trust fund is currently valued at less than $600 million, including difficult to sell assets such as the Carambola resort on St. Croix.

(See “The V.I. Budget Crisis, Part 3: The GERS Time Bomb,” in Related Links below.)

Moody’s also put the territory’s debt on a negative watch, meaning it projects it may downgrade further in the near future.

Other outside analysts have made similar projections that the territory may soon be forced to restructure its debt.

In November, Greg Clark, Debtwire’s head of municipal research, told the Source “a default would be difficult to avoid absent any drastic change in the U.S. Virgin Islands’ outlook.”

Clark said if there is a default, he thinks “it is much more probable, in the neighborhood of 80 percent, that the federal government will set up a mechanism similar to Puerto Rico.”

Normally, a bond downgrade increases the cost of borrowing. Because the private market already declined to lend to the territory in January 2017, this downgrade does not directly change the territory’s position.

The federal government has lent the territory $85 million for budgetary assistance, with $65 million for the central government’s budget. But it has balked at lending more without being placed ahead of the territory’s other borrowers. Tuesday, Collens told senators the V.I. Government failed an additional-bonds test in December that would have allowed the issuance of new gross receipts tax bonds to secure its FEMA loan. If the territory can give the federal government first-lien priority, it might be able to get between $100 million and $200 million, Collens said.

{kind=link}