Tuesday, Fitch Ratings, the debt rating agency, downgraded nearly $2 billion in USVI bond debt for the third time in less than two years. Wednesday, S&P Global Ratings followed suit.

Moody’s Ratings, the third major international credit rating agency, has not yet signaled a new action.

All three agencies downgraded the territory’s debt in 2016 and again in January of this year, in reaction to the V.I. government’s growing debt, unresolved structural deficit and stagnating economy. (See Related Links below.)

Fitch downgraded the territory as a whole, changing its “issuer default rating” – a prediction of how likely the territory was to default on bond debt – by three full notches, from “B” to “CCC.”

Fitch has 10 investment grades: from AAA at the top, for the most credit worthy, to D at the bottom, for entities that have already defaulted on some debt and that Fitch also believes will generally default on most debt.

The first four grades, from AAA to BBB, are considered “investment grade.”

The territory’s CCC rating is seven from the top, indicating it is currently vulnerable and depends on favorable economic conditions, but is not yet “very speculative” nor in bankruptcy or default yet.

All of the individual component bonds were downgraded one grade from “BB” down to “B.”

The bonds are rated two notches higher than the territory as a whole because of a statutory lien on the government put in place in 2016.

“The rating on the bonds is two notches above … reflecting Fitch’s assessment that even though the bonds are exposed to operating risks of the territory, bondholders benefit from enhanced recovery prospects due to the statutory lien on the respective revenue streams for bondholders,” Fitch analysts wrote in their explanation of the ratings action Tuesday.

The lien is on gross receipts tax revenues and federal alcohol excise tax revenues remitted to the territory, aimed at increasing the security for lenders. The V.I. government puts local gross receipts tax revenues under the power of a special, bank-appointed trustee and federal excise tax revenues go directly to the trustee, to pay off interest and principal on V.I. bonds, before any remaining funds will go to the territory’s coffers.

In 2016, the V.I. Legislature enacted the lien after Fitch downgraded V.I. debt and threatened to downgrade further unless a statutory lien was instituted.

“Fitch believes a statutory lien would enhance the recovery prospects for bondholders should the federal government adopt legislation in the future allowing for a restructuring of USVI-backed debt. Failure of the USVI to pass the proposed legislation to create a statutory lien would result in downgrade of the bond ratings,” Fitch officials said in August of 2016.

The Legislature also authorized a bond issuance, but despite the new lien, in January, the V.I. government tried and failed to sell $247 million worth of new V.I. government bond debt. Buyers were not interested.

Fitch cited “significant financial pressures confronting the USVI that are compounded by an extremely high liability burden,” as well as the failure to sell bonds. It said the V.I. government is having a cash flow problem “giving rise to a sizable escalation in accounts payable.”

“While the government has attempted to address this situation through proactive cash management, revenue enhancements and some expenditure reductions, Fitch believes that prospects for stabilization in the USVI’s financial position are limited. Budget imbalance will continue until such time as expenditures, including those related to retiree benefit obligations, are aligned with realistic expectations of future revenue performance, or economic growth well beyond current expectations bolsters revenue sources,” the company concluded.

It also cited problems with the territory’s FY 2016 audit report. That report listed a “$3.7 billion total governmental funds deficit position that captures the long-term pension liability and sizable bonded debt outstanding.”

Fitch officials also said the auditor found “substantial faulty, missing, or inaccurate records that were unable to provide support to the USVI’s financial information.”

Unlike stateside jurisdictions, there is no law allowing the USVI to declare bankruptcy and restructure its debt. But after Puerto Rico missed some debt payments last year, Congress passed the PROMESA act, creating an oversight board and a mechanism for restructuring that territory’s debt.

Fitch also cited concern over the possibility that Congress could expand PROMESA to allow the USVI a mechanism that might restructure its debts.

S&P also lowered ratings on current and future bond debt by two notches, from “B” to “CCC,” for the same reasons.

“The ‘CCC+’ rating on the matching fund notes reflects our view of USVI’s persistent fiscal and liquidity pressures in the face of a continued inability to access the capital markets, as reflected in growing payables despite the adoption of its recent five-year plan,” S&P Global Ratings credit analyst Oladunni Ososami said in a statement about the company’s action on USVI debt secured by federal alcohol excise tax revenues.

Ososami said the same about USVI debt secured by gross receipts taxes. Each type of debt comprises roughly half the territory’s total central government debt load of nearly $2 billion.

Estimates “show the territory could be facing a negative cash balance by the end of August without any additional cash flow management initiatives, which we believe leaves USVI vulnerable to a total depletion of cash before the end of the current fiscal year,” Ososami said.

Many financial experts have begun to suggest the USVI will eventually have to restructure its debts.

“A restructuring is very possible,” Greg Clark, Debtwire’s head of municipal research, told the Source in January.

“During 2017, if they run out of cash, if they can’t sell these bonds, if they don’t have a good five-year plan, I think you could see some additional interest from the federal government,” Clark said at the time.

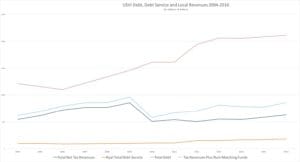

Along with this year’s $110 million deficit, the USVI is facing ongoing structural deficits of around $170 million per year out of a locally funded budget of around $850 million. It has outstanding debt of more than $2 billion, not counting the debts of the government-owned V.I. Water and Power Authority, which is also facing financial problems. It is also facing a $3 billion unfunded pension liability and a pension plan projected to cease being able to pay full pensions by 2023.

The federal government did not move into Puerto Rico until after that territory defaulted on some bond payments. Asked if that made a USVI default and federal government intervention less likely, Clark suggested it may make little difference.

“This time they might move faster because they saw what happened in Puerto Rico,” and if there is a “perceived inability to provide basic government services,” Clark said.

More recently, on Aug. 2, Reuters highlighted the USVI’s precarious financial condition and problems in a widely-printed article that said the territory has “the biggest per capita debt load of any U.S. territory or state – more than $19,000 for every man, woman and child scattered across the island chain of St. Croix, St. Thomas and St. John.

“The territory is on the hook for billions more in unfunded pension and healthcare obligations. But how these islands will recover from years of budget deficits and a severe liquidity crisis remains to be seen,” the Reuters article said.

Meanwhile, the V.I. Legislature has begun budget hearings on Gov. Kenneth Mapp’s proposed Fiscal Year 2018 budget.

The proposed budget has $833.9 million in locally generated General Fund spending; an $11 million cut from his initial FY 2017 proposal. It is a larger, $67-million cut from the budget appropriations ultimately approved by the Legislature. The budget assumes 7.6 percent growth in revenues after the portion of gross receipts taxes set aside for debt service, according to Fitch.

The government increased alcohol, sugar, tobacco, timeshare and net property taxes this year, in hopes of increasing revenues and cutting the deficit.